Whether you are in the planning stages of starting a family or you already have a due date, having a baby will have a substantial impact on your finances. Although some expecting parents astutely prepare their financial house for their newborn, most do not consider all of the ways that a growing family will affect their budget, including income, expenses, and savings.

Outside of death and disability, what can be more stressful and damaging to your social relationships, living situation, and your finances than going through a divorce? It is never an easy process, though it is far more difficult when children are involved.

In the last couple of months, there has been a great deal of uncertainty over the President’s economic plan. The present administration had announced brand new tariffs, delays in implementing them, a “Liberation Day” imposing vast tariffs on global imports to the US, and most recently a 90-day pause in their implementation. We don’t know whether these deep, global tariffs will ever be enforced, but we do know this: They (and the uncertainty surrounding them) have caused unsettlingly large losses in the financial markets.

You’re probably like most of the rest of the country today, working on your personal taxes, and looking forward to moving on with your life! This is the perfect time, however, to start thinking about reducing/limiting your taxable income for the current year.

Our friends and clients know that Isakov Planning Group does not spend valuable dollars on media advertising. Unlike large, national financial advising firms, our most powerful advertisements come from recommendations or referrals from our existing clients. In fact, that is where we get most of our new accounts.

Looking back on 2024, we sincerely thank our clients for putting their trust in us to answer their financial questions and managing their investments. Our joint successes over the past 12 months testify to your confidence in our team and a consultative approach to your financial security.

Anyone can invest in a common stock or in a specific business sector through mutual funds. But even within various stocks, have you considered looking into one that provides substantial dividends, which can add to the value of your stock?

Real-life case studies are proven ways to get consumers’ attention, and perhaps one of the reasons is that people like to see if and how that situation applies to them. We’ll use a case study to illustrate a type of retirement savings scenario that applies to a certain segment of the population. In this instance, people who are actually on track for retirement but don’t realize it.

Artificial intelligence or AI is one of the hottest topics of the decade. Not a day goes by where you don’t see the effects of AI. This month, the researchers who developed “machine learning,” the basis for AI, were awarded the Nobel Prize.

If AI can take vast amounts of information and distill it to answer questions about health care, enhance Web-based searches, and correct grammar, can it help better predict movements and trends in the financial markets? And can that help improve the performance of your portfolio?

It probably isn’t what you think! Most people may answer, “My home, of course.” Not really. Your home may possess significant dollar value, but we believe your most valuable asset is your income. Why? Your income is the asset that fuels financial growth and security.

So, you ran into some extra money and you decided to purchase 100 shares of a stock that you’ve been following. If your intention was to leave that investment alone for a number of years, you are hoping that the share price rises dramatically (assuming it does not pay a dividend), increasing the value of your 100-share purchase. The stock’s share price (and the value of your investment) will generally change only according to the ups and downs of the overall market.

A person’s net worth is not some arcane financial term. It is a living, breathing testament to your financial situation, and it says volumes about your assets and your debt, in addition to how you should be budgeting and planning for the future.

The idea of saving money for “a rainy day” is a founding principle of financial management. Though the advice is as old as investing itself. Putting aside money for unforeseen costs, such as major home or car repairs, sudden job loss, funeral expenses, divorce proceedings, among others, are people really heeding this sage advice? From a real sense, the likelihood of more severe weather is increasing, and a rainy-day fund couldn’t be more relevant today.

Over the past few years, we have discussed important issues and steps you can take to ensure your financial peace of mind. However, we have not directly addressed a basic question: If you made the decision to consult with a financial advisor, why choose Isakov Planning Group?

You may already be saving for your retirement by putting money into a 401(k), IRA, SEP IRA, 403(b), or 457 retirement plan. That’s an excellent, long-term strategy. But you may need to go a step further.

When I talk with people about their existing retirement plan accounts, they generally can tell me two important items: (1) approximately how much money the plan currently holds and/or (2) how much money they set aside each week or month for the retirement account.

As a financial advisor, you meet so many types of people who have an array of financial concerns or issues. In my nearly 20 years in this business, I’ve put together a short list of some of the most common (and important) situations that arise, and how we address them.

Last month, we talked about 2023 results, which forms the backdrop to what could be a busy, complex year for financial decision making. This month, we discuss how these trends will affect how you spend, save, or invest your money in 2024, especially coming into the elections in November.

With the turn of the calendar page, we welcome the arrival of 2024. It’s the ideal time to review a wild 2023 in the U.S. financial markets, driven in good measure by movement on interest rates and inflation.

Under normal circumstances, if you have a conventional IRA or 401(k), you must begin to take distributions from your retirement plan upon celebrating your 72nd birthday (or your 73rd birthday if you reached 72 after December 31, 2022). If you had a conventional IRA, your distributions would be taxed. However, what happens if your spouse or another person inherits your IRA? Do the rules change? The situation becomes a bit more complicated.

With college costs rising well beyond the limits of affordability, the importance of saving today for a child or grandchild’s education expenses cannot be emphasized enough. The investment accounts introduced by the Uniform Transfer to Minors Act (UTMA) and the Uniform Gift to Minors Act (UGMA) are options to traditional 529 plans. What are the differences among these investment tools? Here's what you need to know.

I’m a financial planner, and in my professional opinion, everyone with a job can, and should, put away whatever money they can for their future retirement. After all, it is nearly impossible to live on Social Security payments alone after retirement.

One of the easiest savings decisions you can make is to use one of the investment vehicles offered by so many employers—the 401k. Even if you don’t work as a full-time employee, you can set up a 401(k) plan. The real issue is whether to choose a pretax, conventional 401(k) or a Roth 401(k) plan.

The way you approach your financial decisions reflects your personality. Here’s an important question: How did you react to the market downturn in 2022? Did you change your investment or spending patterns during this time? Here are four types of personality traits that may help define how you make financial decisions.

Imagine this scenario: You and your spouse are planning a vacation, but you are disagreeing about how much you can spend. Your wife or husband believes that you two can afford a 2-week, first-class tour of Europe, but you are thinking more of a 4-day cruise around the Caribbean, because of that new bedroom set you ordered last week.

This type of disagreement (which could become heated) is surprisingly common. It arises because couples don’t spend enough time talking about money. Did your significant other spend money on an expensive dinner at an upscale restaurant, or costly tickets to concerts or sporting events? This can be the subject of simple disputes, which can lead to serious discord over your family’s financial situation. It can also be the start of a rift that may break up the relationship.

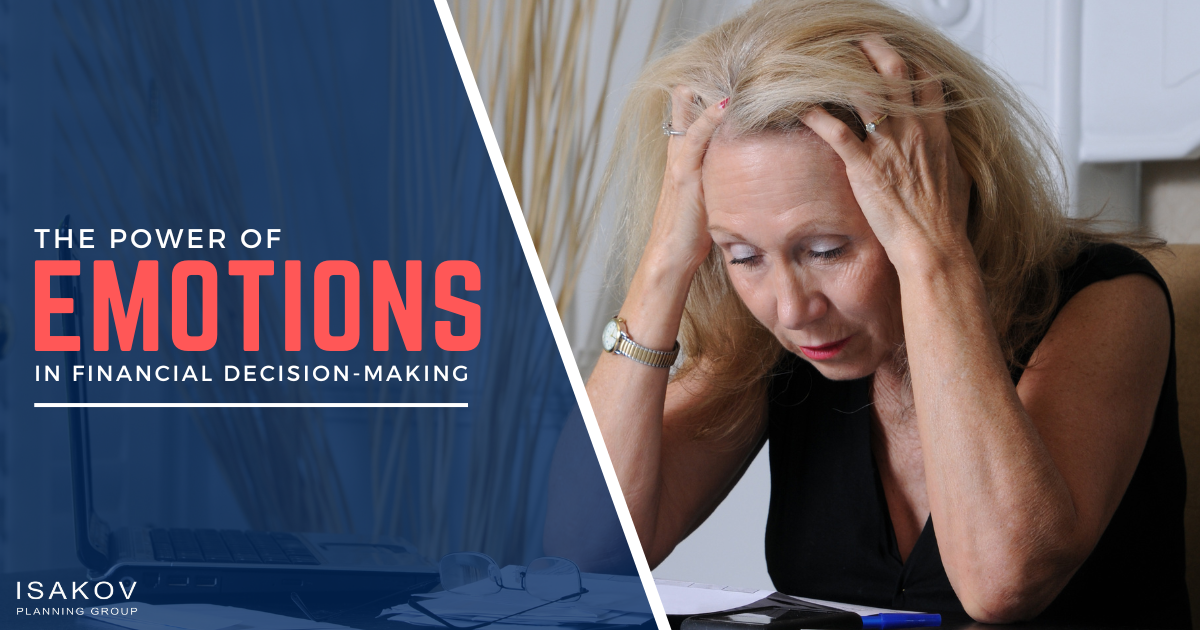

How people spend and save their money is intensely related to an individual’s state of mind.

People who are anxious or depressed may not be in the best position to make optimal financial choices.

Monetary decisions are best made when all of the options have been carefully considered.

That being said, behavioral health does affect how a person approaches financial decision making. After receiving depressing news, who hasn’t thought of going on a shopping spree, because it’ll make you feel better? Spending money can be fun—even uplifting—but it may not be the best choice at that time.

In previous posts, I’ve often mentioned financial plans. What exactly is a financial plan? Why do you need one? Most simply, a financial plan spells out your current financial status and lists your monetary goals for the near future and over the long term. A financial plan also provides a highly customized strategy to attain these goals.